The Definitive Guide to the National Pension System (NPS): Common Scheme vs. Multi-Scheme Framework

NPS common scheme vs multi scheme framework is the most important aspect which helps in deciding how to structure the retirement plan

The Definitive Guide to the National Pension System (NPS): Common Scheme vs. Multi-Scheme Framework

The National Pension System (NPS) has undergone structural changes. Regulated by the Pension Fund Regulatory and Development Authority (PFRDA), the NPS has evolved from a retirement portal restricted to central government employees into a dynamic investment engine available to all Indian citizens.

With the introduction of the modern Multi-Scheme Framework (MSF) alongside the legacy Common Scheme, the NPS now blends sovereign capital security with market-linked growth. This comprehensive guide breaks down the updated rules, asset configurations, tax mechanisms, and strategic differences between these frameworks for both government and private sector professionals.

Part 1: Foundations of the Modern NPS Architecture

The NPS is structured around two primary account variations designed for distinct financial operations: Tier 1 and Tier 2.

Tier 1 (The Core Retirement Vehicle): This is the mandatory pension account that carries strict withdrawal rules but unlocks institutional tax exemptions.

Tier 2 (The Flexible Investment Portal): A voluntary investment account that features no lock-in periods, allowing you to deposit and withdraw capital at will. However, it requires an active Tier 1 account to open and offers no tax deductions, making it significantly less popular than standard mutual funds.

The PFRDA has recently updated the operational parameters for these accounts:

Operational Metric | Tier 1 Account | Tier 2 Account |

Eligibility Age Limit | 18 to 85 years old (Extended from 70) | Requires an active Tier 1 account |

Lock-in Period | Restricted until retirement (or 15-year MSF vesting) | Zero lock-in (Full liquidity) |

Minimum Initial Deposit | ₹500 | ₹1,000 |

Minimum Annual Contribution | ₹1,000 per fiscal year | ₹250 per fiscal year |

Maximum Investment Cap | No upper limit | No upper limit |

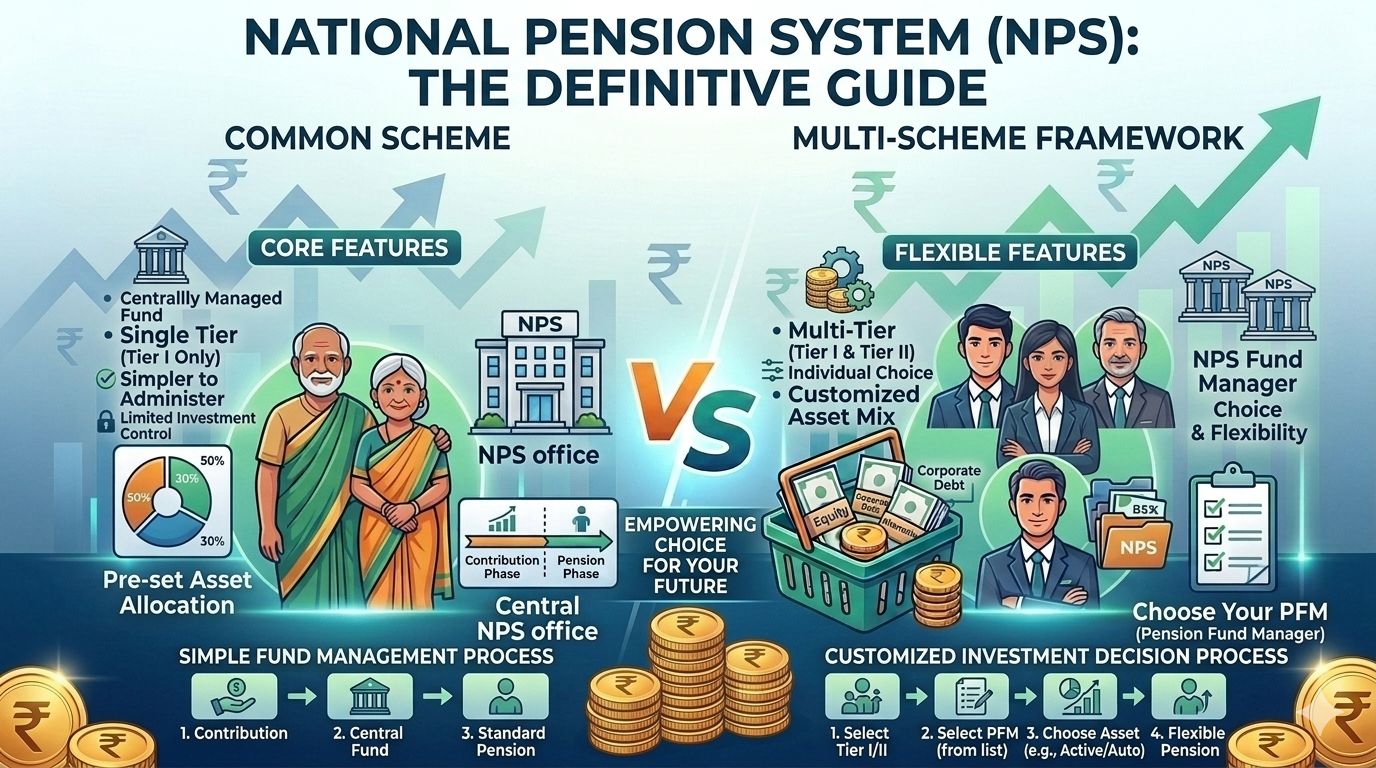

Part 2: The Core Frameworks: Common Scheme vs. Multi-Scheme Framework (MSF)

The structural divide within the modern NPS lies between the legacy Common Scheme and the newly deployed Multi-Scheme Framework (MSF).

1. The Legacy Common Scheme

The Common Scheme remains the default framework for government employees and conservative savers. Under this system, you select a single Pension Fund Manager (PFM) out of the eight approved institutional entities to manage your entire portfolio. You must choose between two investment methodologies:

Active Choice: You manually define your asset allocation across Equity (Asset Class E), Corporate Bonds (Asset Class C), and Government Securities (Asset Class G). However, your equity exposure is strictly capped at a maximum of 75%.

Auto Choice: The system automatically manages your risk profile based on your age. Portfolio choices are divided into three lifecycle configurations: Aggressive Life Cycle Fund (LC75, up to 75% equity), Moderate Life Cycle Fund (LC50, caps equity at 50%), and Conservative Life Cycle Fund (LC25, restricts equity to 25%).

2. The Advanced Multi-Scheme Framework (MSF)

Currently rolled out for the private sector, the MSF introduces institutional flexibility. It removes the single-manager restriction, allowing you to allocate capital across multiple distinct asset classes managed by completely different PFMs.

The MSF permits private sector subscribers to allocate up to 100% of their contributions into Asset Class E (Equity). This alignment closes the historical performance gap between the NPS and equity mutual funds. Furthermore, the underlying asset rules allow Equity funds to hold Gold/Silver ETFs, REITs, and InvITs, while Corporate Bond funds can hold high-yield Infrastructure Investment Trusts (InvITs) to boost portfolio yields.

To protect investors, fund managers under the MSF must offer distinct risk profiles within their equity or corporate bond options: a High-Risk Variant, a Moderate-Risk Variant, and an optional Low-Risk Variant.

Part 3: Maturity, Exit, and Structural Withdrawal Rules

The rules governing final exit payouts have been revised, creating separate operational paths for government and non-government (private sector) professionals.

1. Government Sector Superannuation Rules

Corpus Under ₹8 Lakhs: The subscriber can opt for a 100% lump-sum withdrawal, completely exempt from tax. Alternatively, they can choose to take a 60% lump sum and convert the remaining 40% into a commercial annuity.

Corpus Between ₹8 Lakhs and ₹12 Lakhs: The individual can execute a Systematic Unit Redemption (SUR) to systematically withdraw up to 60% of the capital over a strict 6-year window. The remaining balance must go towards purchasing a mandatory annuity plan.

Corpus Exceeding ₹12 Lakhs: The employee can withdraw a maximum of 60% as a tax-free lump sum. The remaining 40% must be deployed into a compulsory annuity product, providing a recurring monthly pension.

2. Private Sector / Non-Government Exit Rules

Vesting Freedom: Subscribers under the MSF can execute a final maturity exit after maintaining their membership for 15 years, completely independent of their current age. However, a strict lock-in rule applies that you cannot switch your underlying funds or alter manager allocations during this 15-year vesting window.

Corpus Under ₹8 Lakhs: Unlocks a 100% tax-free lump sum exit. Investors also hold the option to take an 80% lump sum and allocate 20% to annuity.

Corpus Exceeding ₹12 Lakhs: Private sector professionals can withdraw up to 80% of their total wealth as a tax-free lump sum, leaving only 20% as a compulsory annuity purchase.

Part 4: Partial Withdrawal, Loans, and Emergency Liquidity

If you require financial liquidity before reaching full retirement, you can access your funds through specific regulatory channels. Partial withdrawals require a minimum membership period of 3 years:

The Cap: You can withdraw a maximum of 25% of your self-contributions only. This calculation completely excludes all employer contributions and any market returns generated by the portfolio.

Frequency: You are permitted a maximum of 4 partial withdrawals up to age 60 (increased from 3), provided you maintain a minimum gap of 5 years between each request.

Approved Financial Triggers: Partial withdrawals are strictly limited to specified life events such as children's higher education/weddings, purchase/construction of a residential house, critical illness medical emergencies, or financing personal skill development, corporate ventures, or formal start-up requirements.

Additionally, subscribers can pledge their accumulated NPS balance as collateral to secure an institutional loan. This loan facility is capped strictly at 25% of your documented self-contributions.

Part 5: Strategic Evaluation: Advantages vs. Disadvantages

Advantages include enhanced investing flexibility via the MSF's 100% equity allocation option, gold/silver asset inclusions, and forced behavioral discipline that locks capital away safely from short-term panic selling. Fund management costs are ultra-low, capped at roughly 0.30% of Assets Under Management (AUM).

Disadvantages include severely restricted liquidity, making it an ineffective tool for short-term personal emergencies. The mandatory annuity clause (forcing 20% to 40% lock-up into commercial insurance products yielding 5-8%) acts as a heavy drag on terminal wealth distribution options.

Strategic Verdict: The National Pension System serves as an excellent foundational tool. You should maximize your investment in it up to the exact threshold where it optimizes your institutional tax breaks (such as corporate restructuring under Section 80CCD (2)). However, your broader financial roadmap should balance this system with direct equity holdings and diversified mutual funds to preserve liquidity and draw down control.

Disclaimer: This article is prepared strictly for general educational purposes and does not constitute formal financial, investment, legal, or tax advice. Please consult a PFRDA or SEBI-registered advisor before finalizing any major investment or portfolio re-balancing decisions.