ETF vs Mutual Fund: 3 Key Differences

When you build a long-term wealth plan, choosing where to put your hard-earned money can feel confusing. Two of the most popular investment options for retail investors are Mutual Funds and Exchange Traded Funds (ETFs).

ETFs vs. Mutual Funds

Which Is Better for Your Investment Portfolio?

When you build a long-term wealth plan, choosing where to put your hard-earned money can feel confusing. Two of the most popular investment options for retail investors are Mutual Funds and Exchange Traded Funds (ETFs).

While they look very similar on the surface — both hold a diversified basket of stocks or assets — they work in fundamentally different operational and financial mechanics.

This guide explains the core differences between ETFs and Mutual Funds. It also covers a useful, lesser-known liquidity feature of Mutual Funds called LAMF, and points out the top asset classes and funds to consider for a balanced portfolio.

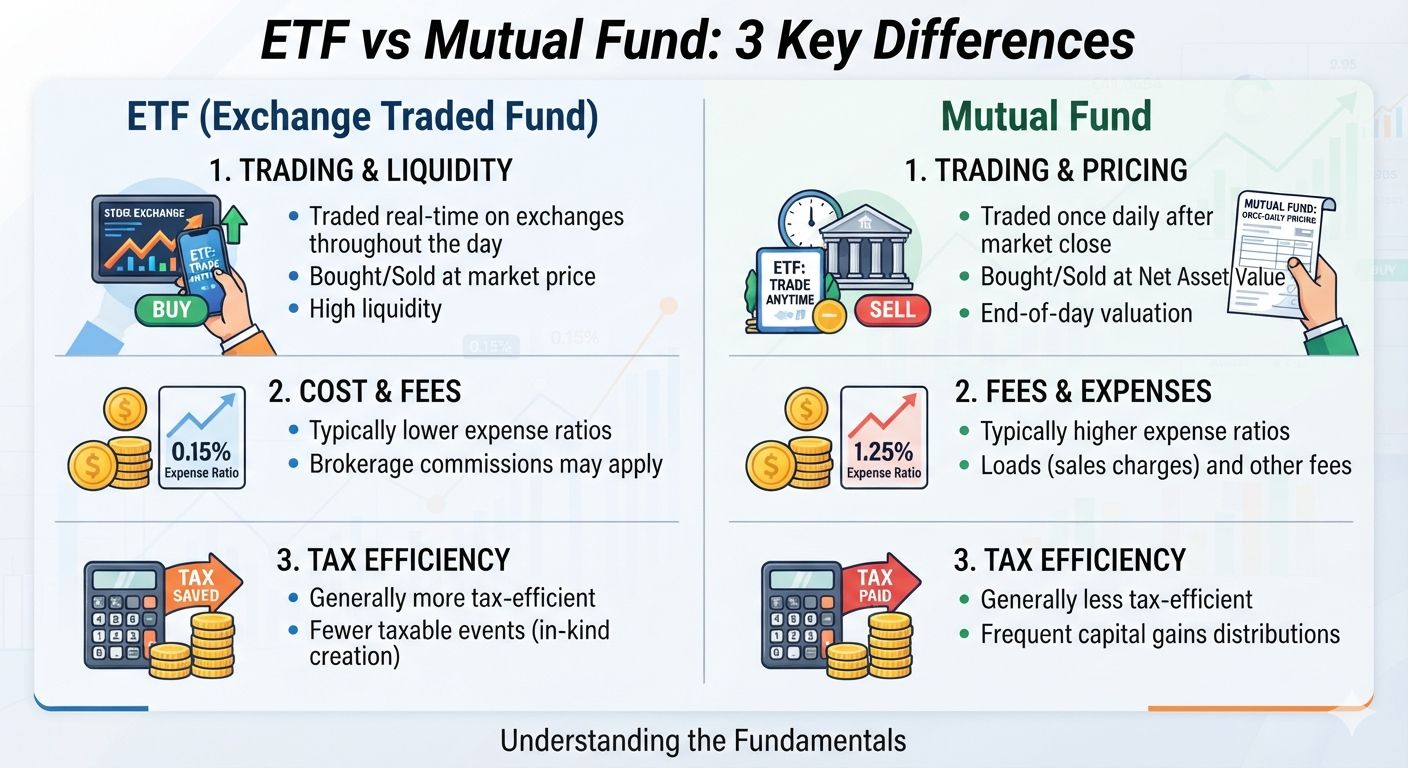

At a Glance: ETFs vs. Mutual Funds

Feature | Mutual Fund | ETF |

Trading | End-of-day NAV | Real-time (live exchange) |

Min. Investment | ₹500 (SIP/lump sum) | 1 unit at market price |

Expense Ratio | Higher (active mgmt) | Lower (passive index) |

Intraday Liquidity | Not available | Available anytime |

LAMF Eligible | Yes | No |

Tax on Exit | Capital gains applicable | Capital gains applicable |

1. What is a Mutual Fund?

A mutual fund pools money from many investors and a professional fund house manages it. For instance, if you invest in a Nifty 50 Index Mutual Fund, the fund manager tracks the index and buys shares of the top 50 companies in India in the same proportion as their weight in the index. If a company's market value shrinks or grows, the fund adjusts its holdings automatically.

The same rule applies to Sectoral Mutual Funds (e.g., Pharma, Logistics, or Banking), where active fund managers research and pick specific companies within that industry, and adjust their weights, to try to beat the benchmark.

The Operational Feature: End-of-Day NAV

Key Insight: You can only buy or sell mutual funds at the end of the trading day. Even if you place a buy order at 9:00 AM, the fund does not process your transaction right away. After the stock market closes at 3:30 PM, the fund house works out the Net Asset Value (NAV)—the value of each unit, based on closing market prices. You get your settlement within T+1 or T+2 business days. |

2. What is an ETF (Exchange Traded Fund)?

An ETF also holds a structured portfolio of stocks or assets (tracking the Nifty 50, international indices, gold, or sectors). But the name explains the main difference: Exchange Traded.

Key Insight: Unlike mutual funds, ETFs trade exactly like equity shares on a live stock exchange. You can buy at 9:15 AM, 11:30 AM, or 2:00 PM at real-time market prices — you don’t need to wait for the end-of-day NAV. Settlement follows the standard T+1 equity cycle. |

3. Mutual Funds vs. ETFs: 3 Strategic Differences

A. Cost and Expense Ratios

Most ETFs simply copy an existing index, so they need very little active management and no large analyst teams. They simply rebalance every 3 to 6 months to mirror the index. As a result, ETFs generally carry significantly lower Expense Ratios than actively managed mutual funds. This saves you a good amount in fees as your money compounds over time.

B. Minimum Investment Amount

Mutual funds usually need a fixed minimum investment (often starting at ₹500 for lump sums or SIPs). With ETFs, you can buy as little as one single unit at its current trading price, which makes it easier for new investors to start.

C. Real-Time Liquidity and Control

ETFs let investors react to price swings during the day. If the market crashes sharply mid-day and you want to capture that specific low point, you can do so right away with an ETF. With a mutual fund, you must accept whatever price applies at the final 3:30 PM market close.

4. The Mutual Fund Advantage: Loan Against Mutual Funds (LAMF)

While ETFs win on intraday liquidity and lower management costs, Mutual Funds hold a big edge that few people use: a financial product called LAMF (Loan Against Mutual Funds).

If you face an urgent money emergency, selling your investments triggers capital gains tax and breaks your portfolio’s growth momentum. LAMF lets you use your mutual funds as collateral for a quick loan instead of selling them or taking an expensive personal loan (which can charge 13%–15%+ interest or more).

How LAMF Works:

> Loan-to-Value Ratio: Up to 45% of the value of Equity Mutual Funds and up to 75% of the value of Debt Mutual Funds.

> Competitive Interest Rates: Often around a fixed 10.75% per year — much lower than unsecured personal loans.

> Interest-Only Repayments: For a ₹50,000 emergency loan, monthly interest is roughly ₹450–₹500. You can repay the principal anytime, with no prepayment penalty.

> No Rigid Credit Score Barriers: Your mutual fund units act as security, so even people with a limited credit history can access this loan.

> Uninterrupted Compounding: Your portfolio stays fully invested and keeps earning market returns even while pledged.

Note: You generally cannot pledge tax-saving ELSS funds (locked in for 3 years) or units held outside the main digital registries. |

5. Notable ETFs to Analyze for Portfolio Construction

Disclaimer: This list shows historical asset performance for educational purposes only. It is not certified financial advice. Please consult a SEBI-registered professional advisor before you invest. |

Important: Never judge a fund only by its trailing 1-year return. Check its minimum 3-to-5-year track record to see how consistently it performs across different market phases.

1. Core Index ETFs (Large Cap Core)

Large-cap index ETFs track the top 50 blue-chip companies in India, and they form the base of a safe equity portfolio. They give strong stability over 10 to 20 years, with historical average returns of 12%–13%. Funds like the SBI ETF Nifty 50 keep very low expense ratios (around 0.04%).

5-Year Historical Average Return: ~15.6%

2. Next-Generation Indices (Mid/Large Growth)

Funds that track the Nifty Next 50 index (companies ranked 51–100 by market cap) give investors access to high-growth companies. Products like the Nippon India ETF Junior BeES see more price swings but tend to make up for it with stronger long-term growth.

5-Year Cumulative Return: Upwards of 125% (more than doubling asset value).

3. Sectoral and Thematic ETFs

If you want to bet on a specific industry, sectoral ETFs give you a liquid option. For example, the Kotak Nifty PSU Bank ETF has captured large cyclical turnarounds in the public banking sector in recent years.

3-Year Cumulative Return: Exceeded 140%.

4. International Tech ETFs (Geographical Diversification)

ETFs that track the US Nasdaq 100 (such as the Motilal Oswal Nasdaq 100 ETF) let Indian investors own a small share of global technology giants like Microsoft, Apple, Alphabet, and Meta.

3-Year Annualized Return: ~23.6% (historically boosted by global tech growth; expect this to settle down over longer periods).

5. Gold ETFs (The Safe Haven Hedge)

Gold has shown strong resilience. It often outperforms equities during market corrections and delivers solid annual returns above 13% over a 10-year period. Gold ETFs remove the risks of physical storage, making charges, and purity, while still giving you instant liquidity.

A simple rule to follow is the 100 − Age Rule: if you are 25 years old, put 25% into safe-haven assets (Gold ETFs, PPF, or liquid instruments) and 75% into equities.

5-Year Cumulative Return: 94% (nearly doubling in value).

Conclusion

If you want to keep fund fees as low as possible, trade instantly at exact prices during the day, and buy small market units, ETFs are an excellent fit. However, if you want a portfolio that can act as security for low-cost emergency loans without forcing you to sell your assets, Mutual Funds coupled with LAMF give you a valuable structural edge. Balance your asset allocation, track 5-year rolling consistency, and keep investment costs low to build long-term wealth. |

Disclaimer: This blog post is meant strictly for general educational purposes and does not offer financial, legal, tax, or investment advice. The author is not registered with the Securities and Exchange Board of India (SEBI) or any other regulatory authority as a certified investment advisor. All data, opinions, and analysis here come from personal study and views at the time of writing. Past performance does not guarantee future results. Every investor must do independent research or seek advice from a qualified, certified authority before investing capital.